Full Underwriting vs Accelerated Underwriting: When to Use Each Path

Full underwriting vs accelerated underwriting paths serve different purposes. Learn when carriers should route applicants to each path and how biometric data is changing triage logic.

Every carrier with an accelerated underwriting program eventually hits the same question: where does the boundary between the fast path and the full path actually belong? The "should we offer accelerated?" debate is over. Most carriers run both paths now. What keeps underwriting VPs up at night is the routing logic, the rules that decide which applicants go where, and whether those rules are drawing the line in the right place.

Gen Re's 2025 U.S. Individual Life Next Gen Underwriting Survey found that 59% of individual life applications across participating carriers were eligible for accelerated underwriting. That number keeps climbing. But flip it around: 41% of applications still route to full underwriting. Where that split lands has real consequences for cycle time, cost per policy, and mortality outcomes.

Munich Re's accelerated underwriting mortality slippage research found that misclassification rates differ by demographic segment, with males, older applicant ages, and lower face amounts showing higher slippage. The routing decision between full and accelerated paths directly shapes the risk profile of each pool.

What separates the two paths in practice

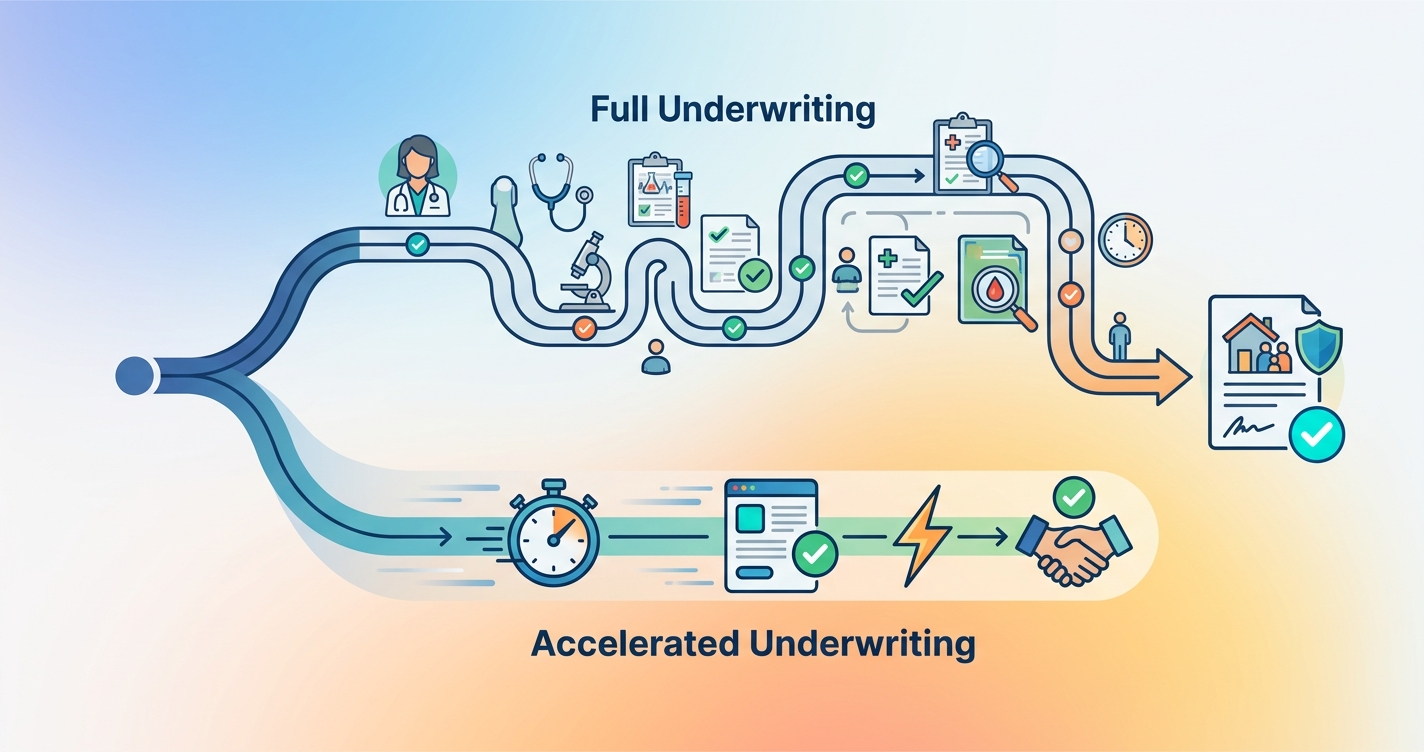

Full underwriting and accelerated underwriting aren't different products. Same policy, different workflows. The path an applicant takes depends on their characteristics and what the data says about their risk.

Full underwriting is the traditional process. An applicant submits their application, and the carrier orders a bundle of evidence: paramedical exam, blood and urine labs, attending physician statements where warranted, prescription history, MIB records, motor vehicle reports, and sometimes credit-based insurance scores. A human underwriter reviews the assembled file, assigns a risk class, and issues a decision. The process takes days to weeks depending on how quickly evidence arrives.

Accelerated underwriting skips the paramedical exam and fluid collection. Instead, the carrier runs the applicant through a rules engine that pulls third-party data — Rx history, MIB, MVR, possibly electronic health records — and makes an automated or semi-automated decision. The applicant never sees a nurse. No needle, no specimen cup. The decision can come back in minutes or hours rather than weeks.

Clean enough on paper. Messy in production.

The routing decision: where carriers set the boundary

Every accelerated program has eligibility criteria that gate access to the fast path. These vary a lot across carriers.

Common eligibility filters include:

- Face amount ceilings — Most programs cap accelerated eligibility somewhere between $1 million and $5 million. Above that threshold, the financial risk justifies the cost and delay of full evidence gathering.

- Age bands — Accelerated paths typically target applicants between 18 and 50 or 60. Older applicants present higher baseline mortality risk, making the abbreviated evidence set less comfortable for pricing.

- Prescription history flags — Certain drug classes trigger an automatic route to full underwriting. Insulin, anticoagulants, immunosuppressants, and certain cardiac medications typically knock an applicant out of the accelerated path.

- MIB codes — Specific impairment codes from the Medical Information Bureau will route an applicant to full review.

- Application responses — Self-reported health history questions can trigger routing. A history of cancer, heart disease, or other significant conditions usually means full underwriting.

The problem with these filters is that they're blunt. An applicant taking a low-dose beta-blocker with an otherwise spotless profile gets the same routing treatment as someone with a complicated cardiac history. The rules can't differentiate because the data underneath them doesn't support that kind of granularity.

Comparing full and accelerated underwriting across key dimensions

| Dimension | Full underwriting | Accelerated underwriting |

|---|---|---|

| Evidence collected | Paramedical exam, labs, Rx, MIB, MVR, APS | Rx, MIB, MVR, application data, possibly EHR |

| Decision timeline | 2-6 weeks typical | Minutes to 48 hours |

| Cost per application | $150-400+ (exam, labs, APS fees) | $15-60 (data pulls only) |

| Applicant burden | High (schedule exam, provide fluids) | Low (answer questions, possibly phone scan) |

| Risk class granularity | Full spectrum (preferred plus through substandard) | Often limited to preferred and standard classes |

| Mortality confidence | High (comprehensive evidence) | Moderate (relies on data proxies) |

| Placement rate impact | Lower (applicants abandon during wait) | Higher (less friction, faster decision) |

| Suitable face amounts | Any, including jumbo | Typically capped at $1M-$5M |

| Suitable age range | Any insurable age | Usually 18-60 |

| Human underwriter involvement | Always | Only for exceptions and referrals |

The economics are pretty clear for straightforward cases. When an applicant is young, healthy, applying for a moderate face amount, and has a clean data profile, routing them through full underwriting wastes money and time. The paramedical exam will confirm what the data already shows. Meanwhile, the delay increases the chance the applicant walks away entirely.

For complex cases, the math flips. An applicant in their late 50s applying for $3 million in coverage with a prescription history that includes statins and a blood pressure medication — the carrier needs more information than third-party data pulls can provide. The cost of full underwriting is justified by the mortality risk that comes with getting the classification wrong.

When full underwriting is the right path

Some risks just cannot be assessed with abbreviated evidence. That's why full underwriting still exists. Carriers that stretch accelerated eligibility too far end up with mortality slippage: the gap between the risk class assigned through the accelerated path and what full evidence would have shown.

Munich Re has been tracking this for years. Their research on accelerated underwriting monitoring shows misclassification isn't spread evenly. It clusters in specific segments. Males showed higher misclassification rates than females. Older applicants showed higher rates than younger ones. Lower face amounts — where carriers historically applied less scrutiny — also showed elevated slippage.

Full underwriting makes sense when:

- The face amount is high enough that misclassification has material financial impact. A preferred-best classification on a $5 million policy that should have been standard represents real money over the life of the policy.

- The applicant's age puts them in a higher baseline mortality bracket. The older the applicant, the more likely that an abbreviated evidence set misses something relevant.

- Prescription or MIB data suggests complexity that third-party pulls alone cannot resolve. A statin prescription in a 45-year-old might mean well-managed cholesterol or it might be the tip of a metabolic syndrome iceberg. Labs and an exam tell you which.

- The carrier's own experience data shows slippage in a particular segment. If post-issue audits reveal that a specific demographic or product combination is generating misclassifications, tightening eligibility for that segment is the rational response.

When accelerated underwriting is the right path

Accelerated underwriting comes down to applicant experience and placement rates. Life insurance has a friction problem that the industry has talked about for decades. Every step between "I want coverage" and "I have coverage" is a point where someone drops out.

LIMRA research has consistently shown that cycle time correlates with placement rates. Faster decisions mean more policies placed. Not because faster decisions are inherently better, but because every day of delay gives the applicant time to reconsider, get distracted, or find a competitor who moves quicker.

Accelerated underwriting works best when:

- The applicant profile is low-risk and the data confirms it. Young, healthy, moderate face amount, clean Rx and MIB history. The full evidence set would tell you exactly what the data pulls already show.

- The product is term life with a modest face amount. The financial exposure per policy is lower, making the cost of occasional misclassification manageable in aggregate.

- The distribution channel demands speed. Direct-to-consumer digital channels, embedded insurance at point of sale, and broker channels competing on turnaround time all need fast decisions.

- The carrier has sufficient volume to absorb some mortality variance. Accelerated underwriting is a portfolio-level bet. Individual misclassifications happen. The math works when the volume is large enough for the law of large numbers to smooth out the variance.

How biometric data is changing the routing boundary

Traditional routing criteria are binary, and that's the core limitation. Pass or fail each knock-out rule, no middle ground. It's really a data problem. The data sources available at triage are themselves binary: has a prescription or doesn't, has an MIB code or doesn't.

Contactless biometric screening introduces continuous variables into the triage equation. When an applicant completes a camera-based vital signs scan during the application process, the carrier gets real-time physiological data: resting heart rate, heart rate variability, respiratory rate, and blood oxygen levels. These are continuous measurements, not binary flags.

That changes routing logic. Instead of binary knock-out rules, carriers can set threshold-based criteria. An applicant with elevated resting heart rate might get routed to full underwriting not because of a prescription flag but because their current physiological state suggests further investigation is warranted. Conversely, an applicant who would have been knocked out based on age alone might stay on the accelerated path if their biometric data looks favorable.

The result is a tighter boundary between the two paths. Fewer applicants unnecessarily routed to full underwriting, and fewer slipping through accelerated who probably shouldn't have.

A 2025 study published in Frontiers in Digital Health examining remote photoplethysmography reported heart rate measurement accuracy above 99% compared to pulse oximetry reference devices, with respiratory rate accuracy at 96% relative to chest belt sensors. The data quality from smartphone-based measurement has reached a level where underwriting decisions can reasonably incorporate it.

The hybrid path: a third option carriers are building

Not every carrier sticks with two paths. Some have introduced a third. This middle tier collects more evidence than accelerated but less than full. It might include an electronic health record pull, a phone interview with a paramedical service, or a targeted lab panel — but not the complete evidence package of traditional underwriting.

The three-path model looks like this:

- Accelerated path — Data pulls only, automated decision, minutes to hours

- Express path — Data pulls plus one or two targeted evidence items, semi-automated decision, days

- Full path — Complete evidence gathering, human underwriter review, weeks

Gen Re's survey data shows growing adoption of this approach. Carriers reported using an average of 10.6 data sources in their next-gen underwriting programs, up from previous years. The increase reflects carriers adding more signals to the triage process — not to slow things down, but to create finer-grained routing that keeps more applicants on faster paths without compromising risk selection.

Contactless vitals scanning fits naturally into the express tier. It adds a real-time biometric signal without adding the scheduling delays and costs of a paramedical exam. The applicant completes the scan on their phone during the application, and the data feeds into the triage engine alongside Rx history, MIB, and other sources.

Current research and evidence

Research on accelerated underwriting outcomes is growing, though mortality experience data is still limited. Most programs haven't been running long enough to generate credible claims data.

Munich Re's mortality slippage studies represent the most comprehensive industry analysis. Their work using random holdout and post-issue audit data from participating carriers has identified that misclassification in accelerated programs is concentrated rather than evenly distributed. The practical implication: routing rules need to be calibrated differently for different demographic segments rather than applying uniform eligibility criteria.

Gen Re's 2025 survey, which included carriers representing over 2 million paid policies and more than $700 billion in benefit amount, found that 94% of respondents tracked accelerated underwriting throughput as a success metric. Mortality slippage was tracked by 81% of respondents. The gap between those numbers suggests that some carriers are still more focused on speed than on mortality outcomes — a balance that will need to correct as books of accelerated business mature.

LIMRA's placement rate research provides the demand-side justification. Their data consistently shows that faster underwriting processes correlate with higher placement rates, which in turn drive premium volume. The business case for accelerated underwriting rests on this dynamic: even if individual policies carry slightly higher mortality risk than their fully underwritten equivalents, the volume gains and cost savings more than offset the difference at portfolio level.

The future of underwriting path selection

The direction is smarter routing, not broader accelerated eligibility. Nobody is trying to put every applicant on the fast path. The goal is getting the right people on the right path, faster.

Contactless biometric data, real-time electronic health records, and better predictive models are all pushing in the same direction: a triage engine that assigns each applicant to the most efficient path that still produces enough evidence for sound risk classification.

Circadify is working in this space, developing contactless vital signs technology that integrates into digital application flows. By adding real-time physiological data to the triage equation, carriers gain another signal for routing applicants between full and accelerated paths — one that captures current health status rather than relying solely on historical records. Learn more at circadify.com.

Frequently asked questions

Is accelerated underwriting less accurate than full underwriting?

It uses less evidence, which means there is some mortality slippage compared to fully underwritten business. Munich Re's research shows this slippage is concentrated in specific demographic segments rather than spread evenly. For low-risk applicants who meet eligibility criteria, the accuracy gap is small. For borderline cases, full underwriting provides materially better risk classification.

Can an applicant request full underwriting instead of accelerated?

Yes, in most programs. An applicant who believes a medical exam would result in a better risk class — someone who is very healthy but has a prescription flag that might limit their accelerated classification — can typically request the full evidence path. Some carriers proactively offer this option.

How do carriers decide where to set the face amount cap for accelerated eligibility?

It comes down to risk tolerance and reinsurance agreements. The cap represents the point where the financial exposure from potential misclassification exceeds what the carrier is comfortable absorbing. Reinsurers also set their own limits on what they will accept through accelerated programs, and these limits often drive the carrier's cap.

Will full underwriting eventually go away?

Not likely. Complex cases, high face amounts, and older applicants will continue to need comprehensive evidence gathering. What is changing is the proportion of applications that route to full underwriting and the efficiency of the full process itself. Digital tools are making traditional underwriting faster even when the full evidence set is required.